monsitj/iStock via Getty Images

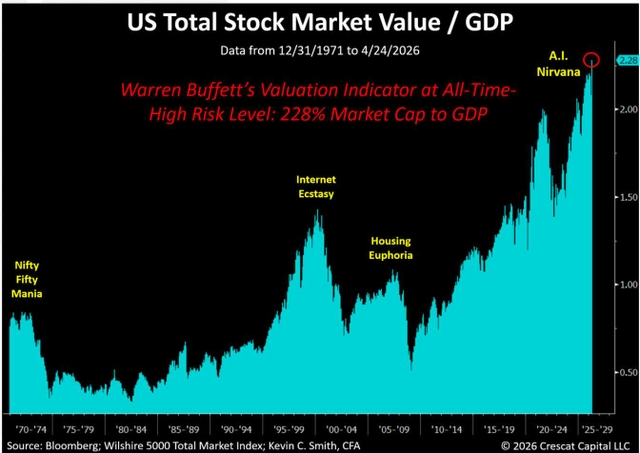

The US stock market is historically overvalued, posing a major potential risk to investors at large. The extent of the bubble is illustrated by Warren Buffett’s favorite valuation risk measure, total stock market value to GDP. It just reached a new high, 228%, 59% higher than it was at the peak of the Internet boom in 2000!

What Could Cause a Crash?

We see three catalysts at play simultaneously:

- Inflation – An oil supply shock caused by the Iran war on top of a metals supply cliff due to years of underinvestment in mining exploration and development

- A.I. Bust – Corporate cash flow and profit destruction from A.I. malinvestment

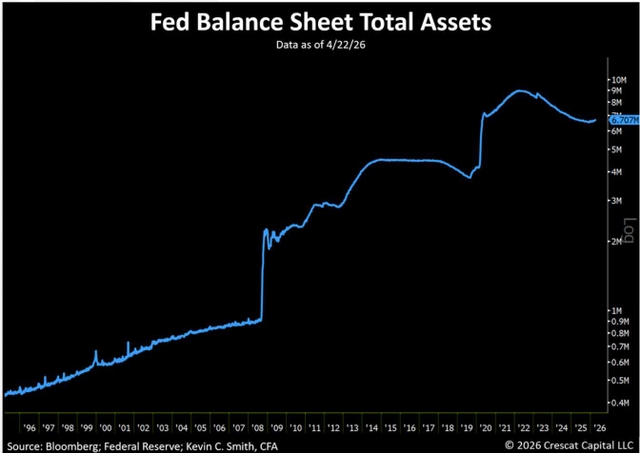

- Monetary tightening – On the heels of Jay Powell’s Quantitative Tightening (“QT”), see the downturn from 2022 in the chart below, incoming Fed chair, Kevin Warsh, plans to reduce the central bank’s balance sheet even more. Never mind that Powell has already started Quantitative Easing (“QE”) again. See the 2026 turn-up in the chart. The Fed has been buying Treasury-Bills and calling this new QE “reserve management purchases” or RMPs, not QE. Don’t be fooled. It’s money printing and a clear indication that the current Fed believes the financial markets need this lubrication. Warsh does not agree.

Each of these drivers has historic parallels including:

- The oil supply shocks that preceded the 1973-74 and 2008 busts

- The Internet capex spending frenzy that drove the 2001 tech bust

- The Fed tightening that led to and exacerbated the Great Depression

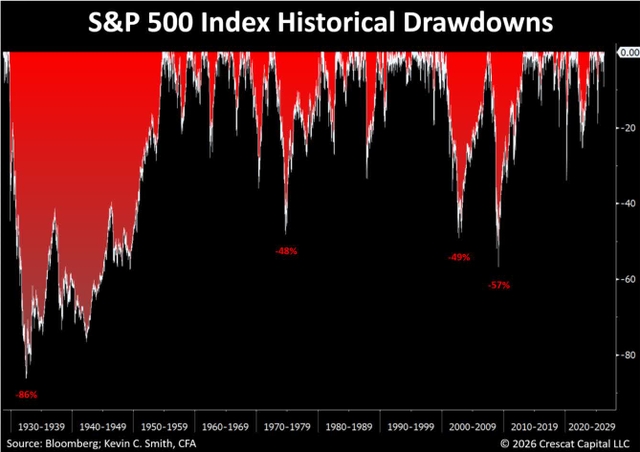

But Crescat, Stocks Always Go Up!

This chart is a reminder that the S&P 500 goes down too, sometimes a lot. The numbers show the max drawdowns of the four biggest bear markets in the index’s history. It’s been almost 97 years since the start of the biggest one to date. The red shaded areas show that amount of time the market spends recovering from a drawdown, just to get back to its prior high.

From all-time highs in price, combined with historic high fundamental valuations, and macro triggers abounding, the risk of a stock market meltdown on the near-term horizon is as high as we have ever seen it.

Manic Swing

On March 31, 2026, US financial markets began to reverse course. This was the start of the rally built on hope that the Iran war may be coming to an end. The S&P 500s 14-day Relative Strength Index (RSI), a momentum oscillator used to identify changes in momentum and price direction, bottomed the prior day at just below 30, by mid-month RSI was back above 70. This marked the second fastest weakness to strength rally in the S&P 500 dating back to 1950.

S&P 500 Fast Paced Weakness to Strength Rallies: April screens second fastest since 1950

Irrational Exuberance

The recent rally comes with notable risks. The conflict with Iran remains unresolved. The Strait of Hormuz has opened and closed, then opened and closed, then opened and closed again. Peace talks have stalled multiple times. Meanwhile, WTI & Brent Crude are still up over 40% compared to before the conflict began.

In our assessment, the market appears to be ignoring these ongoing risks and is pricing in a resolution that has yet to materialize. Meanwhile, the conflict persists, and its longer-term economic and geopolitical implications are uncertain.

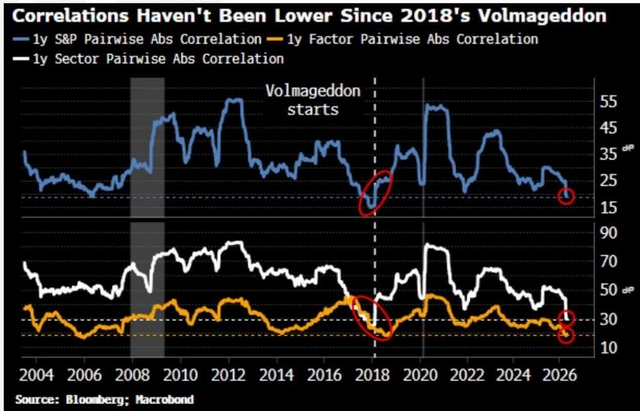

The chart below shows 1-year pairwise absolute correlations of members within the S&P 500 are historically low. In fact, they are the lowest since right before Volmageddon in 2018. This is an indication of complacency with respect to macro risks. Low pairwise correlations mean that over the last year, it has been a stock-picker’s market as opposed to a market where stocks move together based on broad economic events. Low pairwise correlations in low volatility environments suggest investors are ignoring potentially systemic risks.

Buy Gold Mining Stocks and Sell the S&P 500

We think cheap gold and silver mining stocks are still the best countercyclical hedge for the long side of investor portfolios in the current and what we see as likely upcoming macro environment that should be dominated by supply-constrained inflationary pressures. The activist metals portfolio remains the largest long exposure across all our funds. We are tilted toward the smaller cap miners with exploration and development projects that, in our analysis, provide extraordinary value and high growth potential compared to owning the metals themselves. We are short the S&P 500 and Nasdaq 100 through put options in our macro and long/short funds. Of all the macro environments historically, we think the decade of the 1970s most closely represents the outlook for the decade ahead.

Entire 1970 to 1980 Bull Market for Gold Miners vs. S&P 500 – Barron’s Gold Mining Index (BGMI) vs. S&P 500 Index

Though, we think we will also see elements of the Great Depression and the early 2000’s tech bust. These were both times when gold miners outperformed dramatically while the broad stock market crashed.

Dollar/Yen Poised for Decline

We are short the U.S. dollar and long Japanese yen in our macro funds. Long gold though cheap mining stocks remains our favorite way to short the dollar. However, the current setup in the yen is too good to pass up. The 10-year rate differential between U.S. Treasuries and Japanese Government Bonds historically has been a reliable directional indicator for dollar/yen. The Trump administration favors a weak dollar to reindustrialize the country. The yen is the only major currency that has yet to cooperate though the Bank of Japan seems onboard with the plan from an interest rate policy standpoint.

Dollar/Yen vs. UST-JGB 10yr Yield Spread

Crescat’s Performance

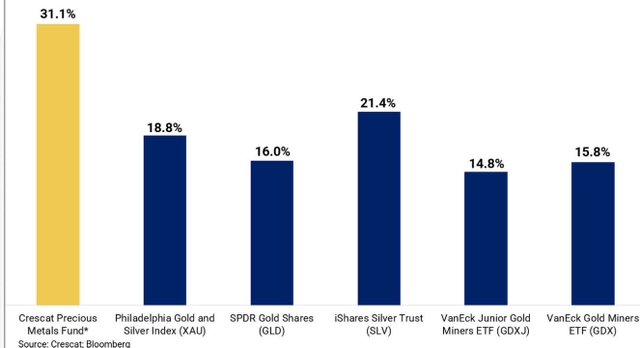

Precious metals mining stocks corrected in March from short-term overbought conditions in February after leading the entire market in 2025 and the first two months of 2026. While our funds were down for the month as a result, we are encouraged to report that all Crescat funds significantly outperformed multiple of the precious metals benchmarks in this pullback. For reference, the VanEck Junior Gold Miners ETF (GDXJ) was down 23.1%, VanEck Gold Miners ETF (GDX) down 20.8%, and the Philadelphia Gold and Silver Index (XAU) down 20.2%. The Crescat Precious Metals Fund has substantially outperformed these benchmarks since inception over five years ago as we show in the chart below. Through March 31, 2026, as it was at year-end 2025, this fund remains the best performing resource-based hedge fund in the eVestment database since its inception, August 1, 2020. We remain highly convicted in our hard asset and precious metals positioning across the firm.

Crescat Precious Metals Fund: Annualized Net Performance vs. Benchmarks Since InceptionAugust 1, 2020 through March 31, 2026 (Estimates)

Crescat Strategies Estimated Net Returns Through March 31, 2026

Crescat hires Bill Pearson, PhD, P.Geo. as Geologic and Technical Advisor

Crescat is pleased to announce that it has hired Bill Pearson, PhD, P.Geo., as Geologic and Technical Advisor to provide professional expertise with respect to the full scope of the firm’s activist metals portfolio. With over 50 years of boots-on-the-ground global mining experience (see his bio below), his addition represents a meaningful expansion of our geologic and technical investment research capabilities.

Bill Pearson is an economic geologist with more than 50 years of experience in the global mining industry. He earned a PhD and MSc in Economic Geology from Queen’s University and a BSc (Hons) in Geology from the University of British Columbia. Bill has led exploration programs across Canada and in 17 other countries, with experience spanning all phases of mining from grassroots exploration through advanced exploration, mine development, and underground and open-pit production across a wide range of geological environments and commodities, including precious metals, base metals, and industrial minerals.

He has held senior executive roles with junior and intermediate mining companies and has served as a director of multiple public companies listed on the Toronto Stock Exchange and TSX Venture Exchange. He is a founding President of the Association of Professional Geoscientists of Ontario and a past director of Geoscience Canada. He received the PDAC Distinguished Service Award in 2015. He has been involved in several notable projects, including Jacobina in Brazil (acquired by Yamana Gold), Central Sun in Nicaragua (acquired by B2Gold (BTG)), and Hope Brook in Newfoundland (acquired by First Mining), and was a co-discoverer of the Iska Iska silver-tin polymetallic deposit in Bolivia, Eloro Resources’ flagship project.

Quinton Hennigh, Crescat’s former Geologic and Technical Advisor, has stepped away from his official role within the firm to focus on his duties as Chairman and CEO of San Cristobal Mining. Thanks to Quinton’s leadership at SCM, this investment has grown to Crescat’s largest and most successful holding across our funds to date. Crescat’s funds are also collectively SCM’s largest shareholder, so we view this move as a positive and logical evolution that is in the best interest of our investors. We maintain a strong relationship with Quinton and are confident that SCM will benefit from his dedicated focus.

Quinton also continues to serve as a director or advisor to many of Crescat’s other portfolio companies. Crescat will continue to engage with him regarding all these companies.

Kevin Smith remains the lead portfolio manager and final decision-maker across Crescat’s five funds. Having expert guidance from seasoned industry professionals, like Quinton and Bill, is an important differentiator for Crescat with respect to its activist metals portfolio.

We are excited to welcome Bill to the Crescat team!

Sincerely,

Kevin C. Smith, CFA, Founder & CEO

Nathaniel Gilbert, Analyst

References

- Net returns reflect the performance of an investor who invested from inception and is eligible to participate in new issues and side pocket investments. Net returns reflect the reinvestment of dividends and earnings and the deduction of all expenses and fees (including the highest management fee and incentive allocation charged, where applicable).

- Performance figures presented Excluding SCM SP represent the fund’s net returns calculated without the impact of the San Cristobal Mining, Inc. side pocket that was designated on July 1st, 2024. The side pocket includes a private equity asset that is not available to new investors in the funds on or after July 1, 2024.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.