Jacob Wackerhausen/iStock via Getty Images

“The riskiest thing in the world is the widespread belief that there’s no risk.” – Howard Marks

On May 9, 1863, about a month before West Virginia officially became a state, the booming oilfield community of Burning Springs fell to Confederate raiders led by Brigadier General William “Grumble” Jones, a Confederate cavalry commander known for his irritable, sometimes profane demeanor. His four regiments of Virginia cavalry burned drilling derricks, production equipment, storage tanks, and thousands of barrels of oil. The raid was part of the Jones-Imboden Raid, a two-pronged Confederate offensive in April and May 1863 intended to disrupt the Union’s important Baltimore & Ohio Railroad in western Virginia (now West Virginia) and counter the North’s political momentum in the region.1

Burning Springs was a “booming” oilfield at the time, producing over 100 barrels of oil per day in 1861. The raid damaged more than 20 railroad bridges, while Confederate troops destroyed thousands of barrels of oil, a loss that would take months to replace. While the attack had little effect on West Virginia’s push for statehood, which succeeded in June 1863, the surprise attack by General Jones did mark the first time an oilfield was targeted in war, “making it the first of many oilfields destroyed in war,” wrote oil historian and author David L. McKain in Where it All Began.2 The Burning Springs raid was notable as the first recorded wartime destruction of an oilfield, but the region’s oil industry eventually revived and boomed across West Virginia.

Just as the 1863 Burning Springs raid disrupted Union supply lines and damaged morale in a divided region, Iran’s current actions in the Strait of Hormuz target global energy markets amid the regional conflict. By closing or disrupting the strait, Iran aims to achieve a similar impact on a much larger scale. The Strait of Hormuz, the world’s most crucial energy chokepoint, saw 20% of global oil trade (crude and products) pass through the Persian Gulf before the war. By controlling the straits, Iran significantly reduced commercial oil traffic, causing one of the largest disruptions in energy markets in history. Four months later, few believed Iran could maintain control of the strait, and many expected oil prices to rise sharply. Surprisingly, oil prices now trade below pre-war levels, despite the severe disruption to oil supplies—arguably the worst in history. Amid the chaos of war, widespread propaganda, and conflicting energy analyses, oil prices continue to drop.

Reflecting on the seemingly illogical current price of oil, one should remember the advice given by the late Richard Russell, who published the Dow Theory Letters for 57 years: “The market can do anything.” Indeed, it can do anything, highlighting short-term unpredictability and the potential for surprising, counterintuitive, or seemingly irrational market behavior. Russell reminded us that investing requires humility—short-term price action is noisy, erratic, and often defies expectations, forecasts, fundamentals, or logic due to factors such as emotions, news, interventions, liquidity shifts, and other influences. Because no one can reliably predict every market twist, investors should avoid overconfidence in short-term calls and focus instead on probabilities and the bigger picture. Russell often contrasted this short-term chaos with longer-term order: over extended periods, more reliable patterns emerge, and certain rules hold. Or as Russell would say, “2 plus 2 has always equaled 4.” Short-term gyrations test emotions and discipline; the long-term picture and probabilities reward patience.

Russell frequently advised against fighting the primary trend or trying to outsmart short-term noise. Just as soon as one thinks they have it all figured out, markets can do anything. Regarding the oil market, higher prices are far from out of the question. The long-term driver behind global oil balance is shut-in production, not seaborne tanker transits out of the Persian Gulf. Every barrel not produced now drains the global oil supply balance either through inventory draws or demand destruction. Since price has not been permitted to rise and destroy demand, the result is an inventory draw. Current outflows from the Persian Gulf consist mostly of already-stranded oil and Iranian oil from floating storage, not new production. It will be interesting to monitor how many oil tankers reenter the Gulf while the world continues to draw down inventories at 5 million barrels per day.

While the Iran war and its aftermath dominate news headlines, a critical market factor often overlooked is liquidity in financial markets. The term “liquidity” is often casually thrown around in market discussions, but little thought is given to exactly what it means. In financial markets, traders speak of high liquidity when everyone seeking money or credit can readily find a sufficient supply. Meaning, traders can exchange stocks, bonds, derivatives, and commodities for money without problems when banks and investors willingly and abundantly extend credit. Liquidity is essential for the smooth functioning of today’s fiat money system, which is literally built on debt. 3

Because debt continues to rise faster than income, sufficient liquidity remains the lifeblood of the fiat money system. In practice, debtors continually expand their liabilities by replacing debt coming due with new debt. Ideally, the new debt bears a lower interest rate, so the debt burden remains manageable for the borrowers. Refinancing maturing debts requires liquid markets to operate smoothly and without issues. Any sudden evaporation of liquidity in the credit markets throws the fiat money system into turmoil and can even cause it to collapse.

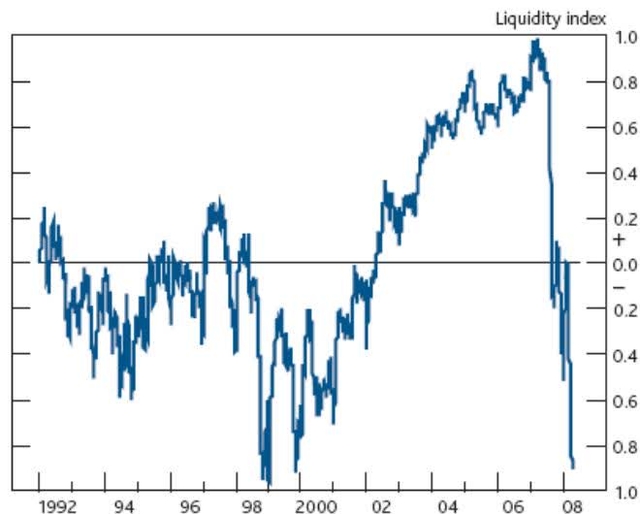

In early 2008, the Bank of England published its “Financial Stability Report,” which included the chart to the right, clearly signaling that liquidity had collapsed. Oddly enough, the report concluded that credit fears were overblown, and banks had overstated their exposure to mortgage-linked investments.4

Sources: Bank of England, Bloomberg, Chicago Board Options Exchange, Debt Management Office, London Stock Exchange, Merrill Lynch, Thomson Datastream and Bank calculations. Index of financial market liquidity. See FSR Chart 3.2 for details.

However, over the following 12 months, the S&P 500 Index lost more than half its value. In response to the liquidity contraction and the stock market’s plunge, the U.S. Federal Reserve aggressively cut the federal funds rate target from 5.25% to near zero by December 2008. The central bank also created multiple emergency lending facilities to unfreeze credit markets and restore market confidence by providing liquidity to banks, primary dealers, money market funds, and short-term credit markets.

In a recent opinion piece in the Financial Times, writer and investor Ruchir Sharma argues that the Federal Reserve needs to do the job it has been failing at for years. That job is to set interest rates at a level that maximizes employment and stabilizes prices. Over time, the Federal Reserve has come to focus solely on employment and to excuse inflation, clearly showing a bias for easy money that has now reached historic extremes. “The economy has hovered near full employment for 55 consecutive months, yet the Fed has missed its inflation target for 63 straight months. Few central banks have matched that record of failure on inflation; in the US, the only comparable episode was during the Great Inflation of the 1970s,” wrote Sharma. 5

Inflation is clearly the bigger problem because it erodes savings and purchasing power over time. More oppressively, inflation acts as a regressive tax that hurts the poor and middle class most, the very groups populist politicians claim to represent. Despite strong jobs data and core inflation over 3%, there is little demand for interest rate hikes. Consumer prices have risen by 30% this decade, making the cost of living a politically charged issue. High prices generate greater pain than elevated borrowing costs. Without persistent inflation, real wages (wages that adjust for inflation) would be rising. For example, the rising number of car loan defaults stems from sharply higher automobile prices, up around 40% this decade, rather than from higher interest rates themselves.

“Liquidity” demands extremely loose financial conditions, a classic setup for capital misallocation. Asset prices, particularly stocks and houses, relentlessly rise, primarily benefiting the wealthy, while the Federal Reserve effectively socializes investment losses through its monetary policy. With financial markets comprising a far greater share of the economy, coupled with growing U.S. budget deficits and total outstanding debt, the economic system is more vulnerable than it was in the 1970s. Any Federal Reserve Chairman hoping to replicate Paul Volcker’s 1980 interest rate hikes would cause far greater damage today. Without most market participants realizing or understanding it, our economy’s dependence on “liquidity” and “easy money” has created a more fragile investment environment.

Antifragility, a concept introduced by Nassim Nicholas Taleb in his 2012 book Antifragile, describes systems or strategies that not only withstand shocks and volatility but also thrive because of them. The Federal Reserve’s long-standing easy-money bias, with persistently low rates and loose monetary policy, has created a fragile financial system. Just as a glass vase can shatter from a small bump, a highly leveraged economy disproportionately suffers from minor market turbulence. Under Taleb’s conceptual framework, suppressing volatility leads to bigger future shocks. By keeping rates too low for too long and excusing inflation, the central bank prevents small, healthy corrections. This indifference, over time, builds fragility, much as Taleb describes how preventing small forest fires leads to massive, uncontrollable future fires.

Low interest rates encourage excessive borrowing and chasing asset prices. This creates portfolios that look fine in calm conditions but suffer disproportionately when conditions change. Financial markets today assume the Federal Reserve (or the President or Congress) will always bail out asset owners. As hard as it is for the prudent investor to acknowledge, that mindset has repeatedly proven correct for several decades. Speculators enjoy their trading gains while system-wide losses are socialized. Just as human muscles and bones strengthen from stress, or one’s immune system benefits from exposure to germs, frequent but manageable financial stress would create a far more robust market-based economy.

Therefore, the investor’s aim should be an investment portfolio that offers a practical way to navigate uncertainty without requiring perfect predictions about quarterly earnings, interest rates, currency exchange rates, credit spreads, or whatever other mindless economic statistic holds particular importance on that day or another. Rather than forecasting the future, the goal should be to design an investment portfolio that gains from Taleb’s ‘disorder’ while protecting against capital destruction.

In Taleb’s 2001 book, Fooled by Randomness, he includes a chapter titled “Survival of the Least Fit – Can Evolution Be Fooled by Randomness?” In it, Taleb explains how the most successful operators in one environment can be disastrous if it changes radically: “Recall that someone with only casual knowledge about the problem of randomness would believe that an animal is at maximum fitness for the conditions of its time. This is not what evolution means; on average, animals will be fit, but not every single one of them, and not at all times. Just as an animal could have survived because its sample path was lucky, the “best” operators in a given business can come from a subset of operators who survived because of over-fitness to a sample path – a sample path that was free of the evolutionary rare event. One vicious attribute is that the longer these animals can go without encountering the rare event, the more vulnerable they will be to it.”

The Lyall’s wren was a tiny, flightless bird that evolved on Stephens Island, a small, predator-free island at the western entrance to Cook Strait, which separates New Zealand’s North and South Islands. The absence of predators allowed the bird to lose the ability to fly and develop a ground-dwelling lifestyle perfectly suited to its isolated niche. Historically, this bird was widespread throughout New Zealand before the land was settled by the indigenous Polynesian people. Scientists theorized that its disappearance from the mainland was due to predation by the Polynesian rat, which had been introduced by the indigenous tribes. This flightless bird thrived on an island two miles from the mainland, which had been connected to the rest of New Zealand during the last glacial period, when sea levels were lower.

Shortly after David Lyall took the position of assistant lighthouse keeper at Stephens Island in 1894, his cat began bringing him birds. Although Lyall had been on the island for only a short time, he could identify most of the birds his cat “Tibbles” brought him, except for one peculiar specimen. This bird was small, olive on the back and pale on the breast, with body feathers edged with brown. Lyall had never seen this bird before — no biologists ever had. 6 Unfortunately, the bird was driven to extinction within months as feral cats rapidly proliferated on the island, illustrating Nassim Taleb’s belief that evolutionary success and apparent fitness are always relative to a specific environment.

When randomness introduces an unforeseen change, such as the sudden arrival of an efficient predator, the very adaptations that conferred advantage in the prior setting become catastrophic liabilities. What survives in one context can be the “least fit” in another, underscoring the fragility hidden beneath apparent optimization. The benign market environment for much of the past seventeen years, including interest rates near zero, U.S. technology supremacy, the dominance of passive investing, and the S&P 500 index repeatedly generating double-digit returns, has created a generation of investors well-suited to the current environment. As a result, today’s investors must remain vigilant to ensure their portfolios evolve rather than remain perfectly adapted to today’s speculative conditions.

Easy access to cheap capital, gross overweighting of US technology companies, and the relentless underlying passive bid have handsomely rewarded those who expect continued double-digit gains in the S&P 500 index. Persistent inflationary trends, coupled with potentially higher interest rates, introduce an unfamiliar predator on portfolios that employ leverage to overweight growth-at-any-price, long-duration technology assets. In our opinion, today’s market is not antifragile—it remains perfectly tuned for an investment environment that may no longer exist. Past performance is context-dependent and not a reliable guide, as every registered investment prospectus warns; extrapolating from past performance ignores the hidden fragilities that accumulate during benign market periods.

Most investors still analyze markets through a post-2008 lens, according to Peter Oppenheimer, Chief Global Equity Strategist at Goldman Sachs Research, who has published a series of papers exploring his “Post-Modern Cycle” thesis. Oppenheimer argues that it may be a mistake not to see that the world is evolving post-2008 Financial Crisis. The world of falling interest rates, abundant and easily accessible cheap capital, and the endless tailwind of globalization is being replaced by something very different: governments competing for capital, nations competing for supply chains, and corporations competing to build the physical infrastructure required for the AI revolution. If this framework is correct, then many of the market’s biggest winners over the next decade may come from sectors that investors spent years ignoring. 7

The tangible, physical economy has been overlooked amid the market’s obsession with headline-grabbing developments in AI, but the virtual world is inseparable from the physical one. Every new AI model ultimately requires data centers, electricity, cooling systems, copper, semiconductors, and engineering and construction expertise. Data centers, power infrastructure, industrial capacity, and supply-chain reshoring back to the United States all require physical investment: pipelines, refineries, utility infrastructure, transport networks, heavy manufacturing equipment, along with a whole ecosystem of tools, pumps, motors, actuators, regulators, gears, valves, sensors, as well as all the necessary process control equipment to actually operate these tangible assets. Companies exposed to these tangible and hard assets should benefit, perhaps meaningfully.

If AI is one source of demand for the “old” economy, geopolitics is another. As the post-Cold War world, dominated by a single unipolar power, begins to splinter into an uncertain multipolar geopolitical landscape fueled by regional conflicts, governments around the world have ramped up defense and security spending. Long-neglected sovereign defense expenditures suddenly appear necessary, if not critical. Post-2008, the financial market handsomely rewarded investors who owned long-duration assets, such as capital-light software companies that did not pay dividends. The post-modern world may reward ownership of scarce tangible assets, productive capacity, and physical infrastructure.

Reality in the physical world must abide by mechanics, limits, and constraints – and depends on energy, materials, logistics, workers, and time lags, writes Craig Tindale in his incredibly informative essays on Substack. 8 The brutal reality is that a great nation must mine copper, manufacture steel, operate refineries, produce fertilizer, balance its electric grid, and sail its own ships. “Workers must be trained, and machines must be maintained.” Nations that incentivize an economy to merely inflate paper wealth rather than direct their capital toward tangible assets that preserve the nation incur consequences. The actual work of repairing and building is slow, technical, and unforgiving. Our country’s cultural obsession with leverage and financialization obscures this reality. A country cannot wish its manufacturing greatness back into existence—it must be rebuilt through serious, habitual reinforcement, which demands competence, restraint, savings, production, engineering, institutional memory, and respect for the physical conditions on which our country’s existence depends.

A nation’s history is shaped by its people who possessed the wisdom to construct, sustain, and defend its ability to produce and manufacture before the crisis appeared. A recent U.S. Navy press release announced that, “After a rigorous, data-driven analysis, we’ve made the tough but necessary decision to inactivate the USS Boise.” 9 Despite the press release’s efforts to spin it as a “strategic move to relocate resources,” our country ultimately abandoned repairs to the Los Angeles-class attack submarine USS Boise (SSN-764). After more than eleven years sitting at a pier and roughly $800 million wasted on a repair effort that never materialized, the submarine will be deactivated rather than returned to the fleet. One must wonder about the real reason why our country could not repair a submarine that it once manufactured and commissioned at a rate exceeding three per year between 1976 and 1996. Perhaps Tindale’s warning should be heeded: “The age of consequences is no longer a future event; it is present.”

As Howard Marks observed, “The riskiest thing in the world is the widespread belief that there’s no risk.” The real risk is that most investors remain unprepared for the new geopolitical and economic landscape now emerging—one of multipolar competition, persistent inflation pressures, supply-chain re-shoring, and surging demand for physical infrastructure driven by AI and defense needs. When Nvidia’s (NVDA) market value is more than twice that of the entire energy sector, the question of when the AI bubble will burst naturally arises. But as value investors have learned over time, bubbles rarely burst when everyone is worried about them.

While many investors remain focused on Nvidia, perhaps the real investment opportunity may increasingly lie in the less glamorous businesses that provide the physical foundations of the digital economy. Still anchored in the post-2008 mindset of easy liquidity, low interest rates, and financialized growth, many portfolios remain optimized for an investment landscape that may no longer exist, leaving them exposed when that environment ends. Perhaps the real investment risk is that many underestimate how much infrastructure still needs to be built. The world is shifting from an era of prioritizing efficiency to one focused on resilience, security, and redundancy. The investment opportunity is that while yesterday’s winners still dominate today’s market, tomorrow’s winners may already exist.

With kind regards,

ST. JAMES INVESTMENT COMPANY

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.