")

Structural skew in the efficacy bell curve of REIT management teams makes it nearly impossible to justify extremely high valuation in REITs.

Welltower (WELL) has been bought up to a valuation that simply does not make sense for a REIT. It is trading at 39X forward AFFO, 43.7X EV/EBITDA and a whopping 205% of net asset value.

S&P Global Market Intelligence

The proffered justification for such a multiple is Welltower’s rapid growth rate along with a widespread belief that it has a superior platform/management.

I disagree with these notions.

Welltower’s growth is within the normal REIT range

The often cited data for Welltower’s superior growth rate is something along the lines of this:

S&P Global Market Intelligence

AFFO grew from $2.84 in 2022 to an estimated $5.32 in 2026.

That is indeed rapid growth.

However, I think the market is mistaken in thinking this is a runrate or otherwise repeatable. If we zoom out a bit, I think it is clearer what actually happened.

S&P Global Market Intelligence

Welltower’s earnings are only slightly ahead of where they were in 2015. Its 10-year growth rate is somewhere around a 2% CAGR.

The rapid growth in recent periods merely represents a recovery in the senior housing sector which is Welltower’s main property type.

Senior housing got massively oversupplied and vacancy rates soared causing operators to have to offer concessions and cut rental rates. All the major senior housing REITs got substantially burned in the downturn. With the level of pain in the sector, developers stopped building senior housing while demographic tailwinds and large nest eggs from a strong stock market began to fill the oversupply.

In the process of filling, rental rates came back up while occupancy rebounded. The combination of higher occupancy and higher rental rates facilitated very strong same-store NOI growth numbers.

S&P Global Market Intelligence

Welltower felt a bit more impact on the bottom line than some of their peers as their senior housing is primarily SHOP (operating properties) while some peers have triple net. The underlying properties are the same, it just impacts when the REIT feels NOI changes. For SHOP, the REIT collects the changes in real-time whereas triple net gets the benefit when lease contracts roll over.

Thus, Welltower’s perceived outperformance is mostly a factor of 2 things:

- Recovery from a deep trough in senior housing

- Timing advantages of SHOP over NNN

In my opinion, Welltower is a perfectly fine company, but nothing out of the ordinary.

Does Welltower have a superior platform/management?

Shankh Mitra had the benefit of becoming WELL’s CEO on October 5th, 2020. For those of you who follow REIT history, this was near the rock bottom of the REIT market after REITs got clobbered by COVID and before the extreme REIT surge in 2021.

When he took over, WELL was trading at ~$56.31.

SA

So the stock has nearly quadrupled in his tenure.

The market seems to have a bad habit of attributing stock performance to management. Management can only control a company’s fundamentals while the stock is influenced by so many outside variables.

I attribute the stock price gains to 3 factors:

- General REIT recovery from the COVID trough.

- Senior housing recovery (detailed above)

- Momentum as WELL became grossly overvalued

The REIT level tailwind was strong from October 2020 through the end of 2021.

SA

When combined with the fundamental recovery in senior housing, WELL nearly doubled by the end of 2021 since Mitra’s coronation.

From there, fundamentals continued to be strong on continued senior housing recovery and then momentum took over. The market started treating Mitra as infallible and there became this assumption that Welltower was somehow cut from a different cloth.

This is perhaps best highlighted by a recent quote from Welltower’s CEO Shankh Mitra at the CITI Property CEO Conference:

“By being the virtue of being a REIT, majority of people who grew up in this industry have learned only to look at things 12 months out, 18 months out. And that sort of created an interesting situation where people don’t know how to value compounders, right? So that’s my perception because not a lot of companies have been compounders in REITs, at least not for the last 10 years. So if you really want to understand our company, understand what the company, I would suggest you look at understand what the earnings power of the company is years out, not just 12 months out.”

In essence, he is saying that Welltower stands alone as a compounder amongst a sea of REITs that are linear by comparison.

I posit that the only thing that has “compounded” is Welltower’s market price while the fundamentals are entirely in-line with REIT peers as we showed above with the ~2% 10-year CAGR.

Frankly, I don’t think it is possible for a REIT management team or platform to outperform at an exponential level. There are many examples of previous hero worship in REITs and they seem to always come back down to earth.

Debrah Cafaro of Ventas (VTR) had a similar start to Mitra in that she became CEO of Ventas in March of 1999. It so happened that healthcare REITs had recently crashed as many of the sector’s loan portfolios failed or otherwise became impaired (healthcare REITs were closer to mREITs at the time). Cafaro came in near the trough as VTR was down 72%.

SA

The sector recovered and VTR stock quickly traded up to 5X where it was when Cafaro took over. By 2013, Cafaro was broadly hero worshipped. She began winning various awards and VTR was trading at too high of a multiple.

The taper tantrum of May of 2013 marked the top of Ventas and it is still trying to get back up to that peak.

Cafaro was and remains a perfectly fine CEO. The point is that the extreme performance was cyclical and sector level factors that are largely outside of the control of management.

We have previously highlighted Realty Income (O) as the subject of similar hero worship. O has always been a reasonably well managed triple net REIT, but there was a period of time when it was regarded as infallible. It was objectively very similar to the other triple net REITs but was somehow thought to be better at a molecular level such that it traded at a far higher multiple than peers. It too came back down to earth, still trading below where it was in 2022 when we wrote about it.

Hero worshipping, or the pouring of capital into companies managed by what is perceived to be exceptional CEOs is uniquely bad in REITs.

In tech, for example, it has often turned out fairly well to just invest unlimited amounts of capital with CEOs who have some sort of special sauce.

Steve Jobs, Jensen Huang and Elon Musk are obvious examples where the market invested at valuations that did not make rational sense, yet it worked out fairly well for most investors. I think the difference is that tech is based on ideas and ideas can have extraordinarily high ROIC. In that manner, a visionary CEO or more likely the combination of the CEO with a phenomenal team of engineers, can legitimately create massive amounts of value.

REITs are different because REITs are based on capital rather than being based on ideas.

The ROIC on purchase of a property is largely bounded. Properties are priced based on current NOI and expected growth. A really strong management team might be able to spot properties with better growth potential than that for which they are priced. However, the delta would only be 200 basis points in an extreme scenario and probably closer to 10-50 basis points of extra value generated by supreme property selection.

It simply isn’t feasible for a CEO to buy at a 15% cap rate when prevailing cap rates are 6%. There is no level of skill that makes extreme outperformance possible. This brings me to a core concept of why hero worshipping is almost always going to be a bad result for REIT investors:

Structural skew in efficacy bell curve of REIT management teams

Due to the capital-intensive nature of real estate discussed above, it is not all that feasible for a REIT management team to generate extreme alpha. In contrast, it is entirely possible for REIT management teams to generate massive negative alpha. There are countless ways that CEOs have torpedoed their companies:

- Excessive share issuance

- Excessive compensation

- Churning properties to no real upside

- Poorly conceived M&A

- Fraud

- Excessive use of leverage

- Et cetera

As such, the bell curve of CEO performance has a fat tail on the left side and almost no tail on the right side.

2MC

The best REIT management teams are those who are consistently solid. They operate with integrity and consistently make wise acquisitions and dispositions. If we were to fill out this graph with historical examples, it is fairly easy to fill up that fat left tail.

- Fraud allegations collapsed ARCP’s stock price.

- Ashford was one of the best performing hotel REITs until management decided to strip the company into 3 pieces and take huge compensation from each piece. It never recovered.

- RMR externally managed REITs consistently underperformed their property sectors

- Macerich (MAC) management refused to sell to Simon Properties (SPG) at around $90 per share. It sits today below $20.

Each time the market has thought a REIT management team was far on the right side of this graph it has not worked well. A REIT simply can’t turn 50 cents into a dollar overnight. That just is not how properties work. They generate cashflows and appreciate consistently over time. It is the cashflow that compounds and it is a long process.

Yet, when investors are buying Welltower at 205% of net asset value they are implicitly demanding that Shankh Mitra turn 50 cents into a dollar.

He seems like an entirely fine CEO to me. He is intelligent and competent, it just isn’t a realistic possibility. Given the extraordinary valuation at which WELL trades the best thing the company can do is issue as much equity as possible at these absurd prices. Every dollar raised with the stock at this level can easily be accretive.

With an AFFO multiple of 38.9X, the dilutive cost of equity capital is 2.6%. You can buy basically any property at that cost of capital and AFFO/share will go up. Welltower is correctly issuing a ton of equity.

S&P Global Market Intelligence

That is tens of billions of dollars raised. Any property purchase is accretive with a 2.6% cost of equity capital, the challenge is just getting it spent.

Real estate acquisition is a very labor intensive process. One has to know the submarket and underwrite all aspects of the property. Thus, to put this much capital to work in a timely basis, Welltower began automating certain aspects of the underwriting process.

They developed an AI driven capital allocation engine that presumably helps allocate capital efficiently and quickly. Public Storage (PSA) recently licensed use of this engine from WELL.

“This data science-driven capital allocation engine is designed to dynamically direct capital to the highest risk-adjusted return opportunities across acquisitions, developments, dispositions and lending.”

I am a bit skeptical of AI or automated data science being able to select which properties to acquire. There might be some value here in cost savings, but it is not the source of WELL’s growth.

The real source of AFFO growth beyond the cyclical recovery in senior housing is issuing capital at an absurd valuation.

WELL’s growth is issuing capital at 205% of NAV and 38.9X AFFO. Any purchase is just automatically accretive.

WELL is correct to use this growth lever for as long as they can.

Investors are not correct to provide this capital.

Capital markets are fickle. Multiples can change overnight and as soon as WELL’s valuation drops back down to a reasonable range, the virtuous cycle of using its high multiple as a currency is gone.

When that happens, the AFFO growth, beyond the remaining SH recovery is also gone. Investors might regret having invested at 205% of NAV.

The other problem with hero worship

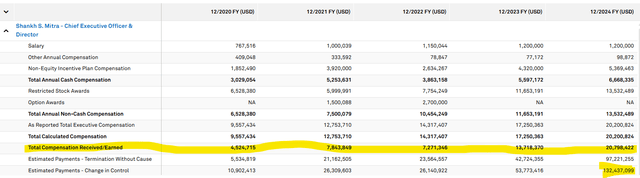

As CEOs garner universal praise, their salaries tend to go up.

S&P Global Market Intelligence

Shankh Mitra was initially signed at a $4.5 million total compensation which is quite normal for a large cap. As his reputation grew, the pay package soared to $20.8 million in 2024. To top it off, he has a $132 million golden parachute if the company is sold or a $97 million severance package if fired.

Welltower is a large enough company that this pay package is not back breaking, but it does take a bite out of earnings.

The bottom line

Welltower is a fine company and senior housing is a reasonably strong asset class that is currently in a cyclical upswing.

At a reasonable valuation, Welltower could make a great investment, but WELL is trading at more than double the valuation of other REITs.

As of 3/16/26, the median REIT trades at 15.6X AFFO and 81.8% of NAV.

I don’t think it is possible for a REIT management team’s sauce to be so special that 39X AFFO and 205% of NAV is worth it.

Buying at this level or participating in any share offering is asking management to turn 50 cents into a dollar… I am skeptical of those chances.