Andrii Yalanskyi/iStock via Getty Images

“The investment world is changing. The lessons learned in the stupendous global bull market of the last 40 years will serve us very poorly in the years ahead.”

Rob Arnott

The latest on passive investing

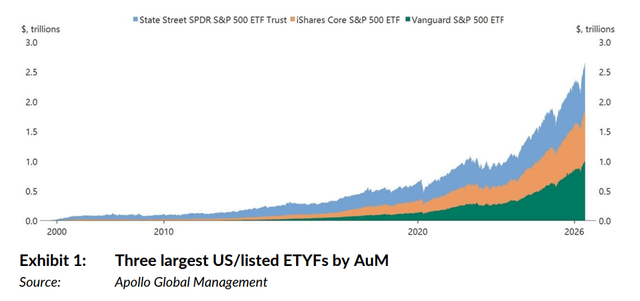

The three largest passively-managed S&P 500 funds now hold a combined $2.6Tn of AuM – an all-time high – with the largest of the three, Vanguard, having just passed $1Tn on its own (Exhibit 1). This shall require a comment or two, which is what this month’s Absolute Return Letter is about.

My (in)famous 2018 book

The title of this letter has been borrowed (with gratitude) from Torsten Sløk, Chief Economist at Apollo Global Management, who recently commented on the phenomenon. His astute observation (one of many) reminded me of the book I published back in 2018 – The End of Indexing. In the book, I argued that passive investing will soon be replaced by a more active approach, and I went through all the reasons why I thought so.

Now, six years later, passive investing is more widespread than ever (see Exhibit 1 again), so you would be forgiven for thinking that I have more than a bit of egg on my face. And maybe I do. That said, here in Denmark, we have a proverb that goes approximately like this: “He who laughs last laughs the loudest”. Do you know what I mean?

Why active equity managers are not as bad as their reputation

Before going any further, allow me to kill a widespread belief which, in my opinion, is plain wrong. When I ask investors why they invest passively, a very high proportion provide the same answer: “Because active managers underperform”. Active managers as a collective group cannot underperform! Equity management is a zero-sum game, i.e. for every investor who underperforms somebody must outperform (before costs). In other words, if you parked your money with an equity manager who underperformed, it was because you picked the wrong active manager – not because all active managers are poor.

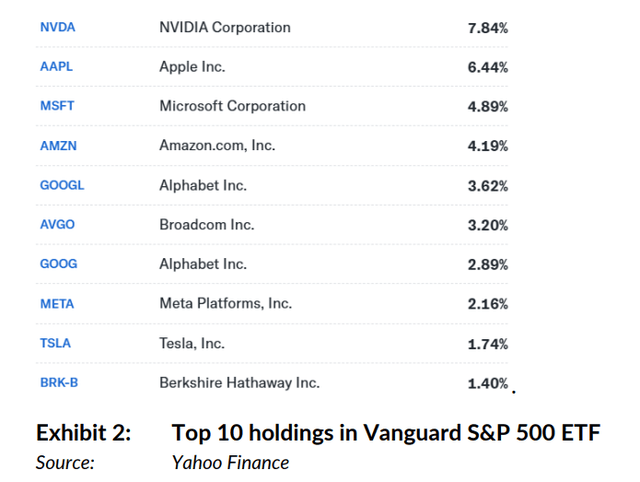

However, that is, in itself, not a reason to go active. I fully understand those investors who struggle to identify equity managers who actually do a decent job. Usually, the best are not the loudest. By investing passively, at least you know that you won’t underperform, but that brings me to the biggest issue I have with passive investing. By investing passively, you always invest in yesterday’s winners, and I prefer to invest in tomorrow’s winners. Take a look at Exhibit 2 below. As you can see, the top-10 holdings in the Vanguard S&P 500 ETF at present are (not surprisingly) all the usual suspects.

Because Big Tech has performed so well in recent years, indices like the S&P 500 are heavily skewed toward this group of companies. As I write these lines, the top-10 holdings in the index account for 38-39% of the total. However, history suggests one industry never remains the biggest forever. Never!

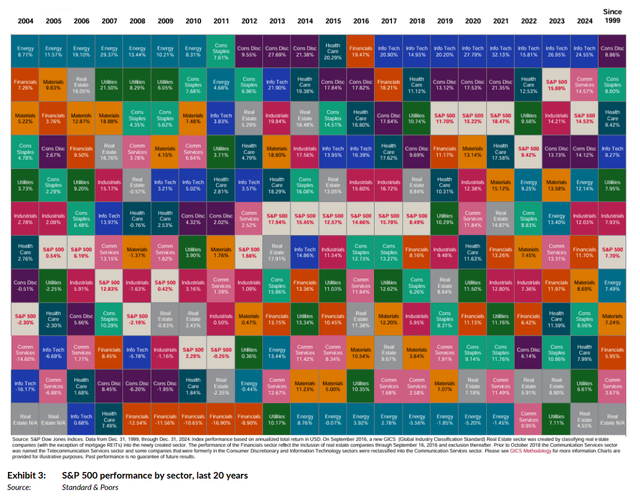

Take a look at Exhibit 3. In 2024 (2025 has not yet been included), IT was, yet again, the best performing sector in the S&P 500, i.e. IT has now, for nine consecutive years, been the top-performing sector in the U.S. Exhibit 3 only covers the last 20 years. However, data going back to 1900 suggests that the S&P 500 powerhouses have rotated regularly over the decades.

Going back to Exhibit 3, as you can see, just in the last 20 years three sectors have dominated – energy in the years before and after the GFC, followed by consumer discretionary for a handful of years before IT took charge, There are obviously no hard rules which dictate this, but could IT’s day in the sun fast be approaching sunset?

This raises the obvious question: What is likely to be the next sector at the top of the pyramid? Back to the point I made about “no hard rules” earlier. AI is truly unique – both in the positive and the negative sense of the word. It is therefore not impossible for IT to dominate for another few years. Having said that, my money is on commodities to outperform equities over the next 5-10 years, and guess what, at present, the most undervalued commodity sector vis-à-vis equities currently is energy.

Other observations

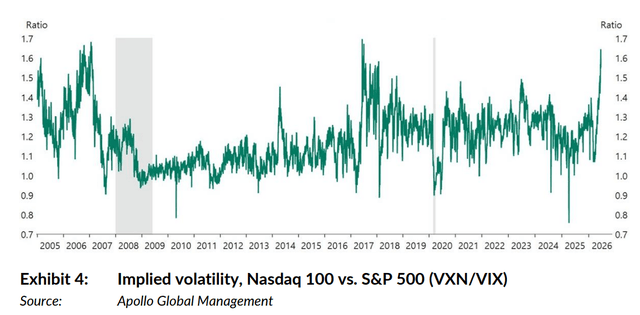

A couple of other observations back up my concerns. Take for example the signal sent by options markets, where volatility in the tech-heavy Nasdaq 100 index has spiked to the highest level for years, whereas volatility in other stocks is still modest (Exhibit 4). This tells me that options markets are bracing for a shakeout in tech stocks, which will be tremendously damaging for passive investors, most of whom have invested massively in high tech.

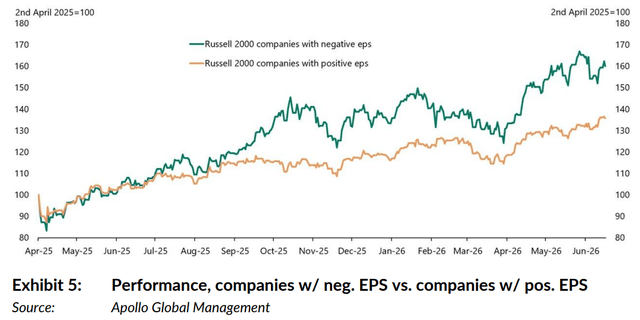

A second observation: Something is not right, when companies with negative earnings keep outperforming companies with positive earnings (Exhibit 5). One could argue that this phenomenon is not necessarily linked to the oncoming tsunami of passive investing, but there is an important link. When you invest passively regardless of price, momentum becomes the driving factor, and that is also the case when you prefer companies with negative earnings over companies with positive earnings. When something like this happens, it always ends in tears. Always!

What should you do?

Going back to the title of this Absolute Return Letter, what does it all imply? Effectively, it implies that humans are increasingly detached from the pricing of U.S. equities, that computers driven by formulas rather than company fundamentals dictate the pricing. Is that good? If you ask me, no, it is not, but opinions vary on this.

Everything is fine until it is not. When the lights are suddenly switched off, the same computers which kept buying will now keep selling, and fundamentals will (continue to) be ignored. That could be a fantastic buying opportunity for investors with cash.

How should you position yourself? The easy, but not necessarily the optimal, option is to stay completely away until the selloff hits us. You will look very smart when all the wheels come off, but you’ll also have missed an awful lot of upside in the meantime (unless it happens tomorrow morning). I have seen quite a few bearish equity managers go out of business before being proven right.

Another option, and the one we pursue, is to invest a substantial part of the assets in sectors which are not represented in the major indices. The risk with that strategy is that you could meaningfully underperform as long as the index funds run the show, but that is a risk I am comfortable with.

A third option is to set a few % of NAV aside every year for hedging purposes, and then continue to buy the types of names listed in Exhibit 2 as if there was nothing to worry about. That will cause you to underperform a little bit (reflecting how much you spend on hedging), but you’ll be well protected, assuming you are hedged correctly, when the boom turns into a bust.

Final few words

Timing? This is the most difficult part of this ‘little’ exercise. It is, in fact, almost impossible to anticipate when the lights will be switched off. I have been through quite a few crashes in my many years in the industry, and I have still not discovered a trustworthy ‘alarm bell’. I follow a few signals such as the ones mentioned in this letter, but there is no single, foolproof formula.

With those words, let me wish you a most enjoyable summer. I never write in August,

i.e. the next time you’ll hear from me will be in early September. As it happens, and because the topic I have covered today is so important, the September Absolute Return Letter will cover the same topic, albeit from a different angle. The working title (so far) is The AI Capex Race. This is a massive topic that shall require more than a few days of work so, while you’ll probably spend the summer in or near the swimming pool, my summer will be allocated to research. My skin can’t tolerate too much sun anyway!

Niels

1 July 2026

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.