Olemedia/E+ via Getty Images

Bitcoin is not ” yield-generating”. It becomes so in certain on-chain contexts as some DeFi lovers teach us, but it is born as an “unproductive” structure. Funds like YieldMax Bitcoin Option Income Strategy ETF (YBIT) try in some way to distort this condition of theirs, using options to generate weekly distributions that, if projected over 1 year, lead to unthinkable “conclusions.”

But what is the degree of sustainability of certain strategies? And above all, what does YBIT give in return for these distributions? Let’s try to answer these questions.

Intro and Definition

YBIT is an actively managed ETF issued by YieldMax, with advisor Tidal Investments LLC, an expense ratio of 1.02% and Net Assets of $35.07 million at the time of this writing (still not too mature). The fund does not invest directly in Bitcoin. It invests in options on selected ETFs (“Underlying ETP”) that in turn offer exposure to Bitcoin (e.g. IBIT), or through synthetic long exposure (which uses US Treasuries as collateral). Then it sells OTM calls (strike 0-15% above the current price) to generate a premium, limiting upside participation (covered call writing). It can alternatively also implement a covered call spread strategy.

YBIT: profile (Seeking Alpha)

There is no traditional benchmark declared in the sense of an index to replicate, but precisely because of its composition the natural comparison is made with IBIT, although there would be inconsistencies here too. In fact the primary objective stated in the prospectus is to generate current income; exposure to the price of the Underlying ETP is a secondary objective.

In fact, the most recent data shows a distribution rate of 38.98% distributed weekly against a 30 day SEC yield of only 2.12%. Distributions that for over 90% of the last 19a have at least 97% ROC. These figures of course will change over time, but are illustrative of the kind of yield this ETF can have.

What Does YBIT Do?

The fund aims to generate a premium from the options sold (covered calls and covered call spreads) on the IBIT ETF. The 30 day SEC yield is the result of exposure to the collateral, which being a treasury is fruit-bearing. The result of this mix changes over time, in fact there has been quite a bit of discontinuity. In part because it naturally depends on the fruits of the strategy and therefore on management’s choices.

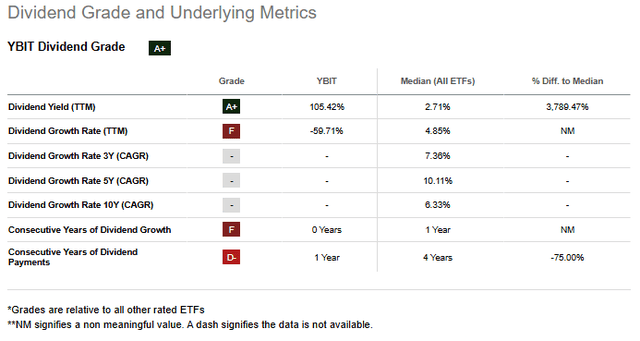

YBIT: dividend grade (Seeking Alpha)

On the downside instead, the prospectus is clear that losses on the downside are not compensated by the premiums collected, except partially. Taking this into consideration, the most suitable role is that of a tactical/satellite component to generate cash flow, not a core investment or a substitute for direct exposure to Bitcoin. In my research I used the metaphor of the “scale” which in my opinion fits well: so let’s imagine a balancing scale, on one side the distributions, on the other the price return; naturally the more weight is loaded onto one of the two sides, for example with a higher distribution, the less these ETFs remain conservative instruments of value (in terms of price), so in my opinion the less they become suitable substitutes for the core component, and the more they become tactical allocations tied to specific market phases.

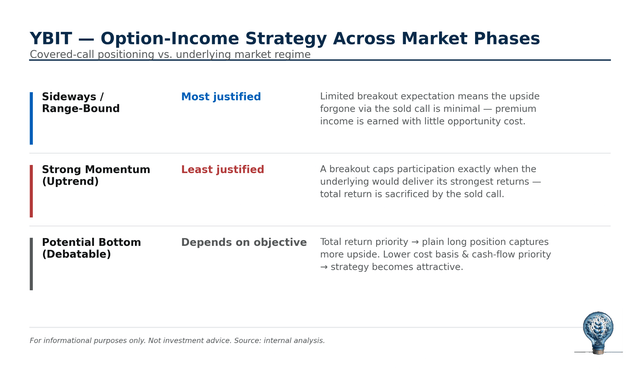

YBIT: strategy (Author)

If market timing logics were introduced, when do these strategies make sense?

Potentially when the underlying is in a sideways phase.

They lose competitiveness in full momentum phases. At that moment the price gains from the restart get “cut” precisely by the call sold.

On one hand, taking a position at the lows increases the weight of the upside cap. But, on the other hand, if the objective is to optimize cash flow, taking a position at low average entry prices is not a wrong thing to do.

Who Is YBIT For?

At this point it’s also easy to better outline the profile of the investor who looks at YBIT: potentially, we’re talking about an investor with a moderately bullish view on Bitcoin, because needless to say the profitability and sustainability of the strategy depends on Bitcoin’s appreciation and volatility. In terms of asset allocation, it is considered a cash-generative instrument, but the total return will depend on entry timing and (not trivially) on the distribution reinvestment strategy (if provided for).

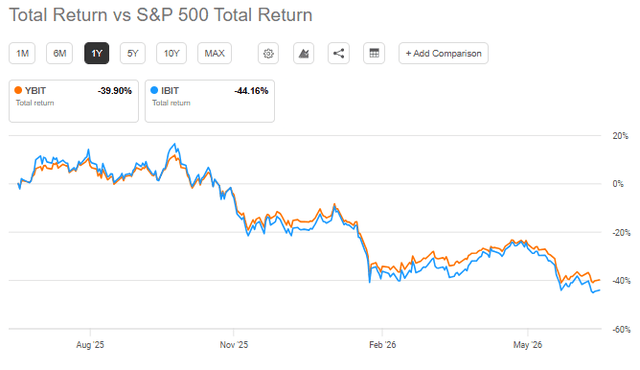

YBIT: Total return (Seeking Alpha)

How Is YBIT Built?

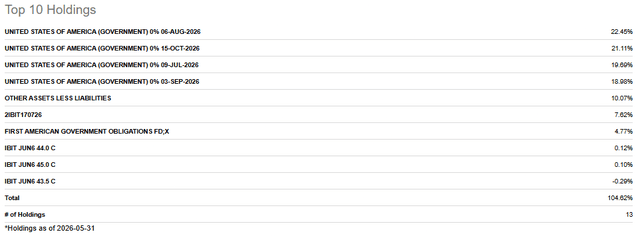

- The composition?at least 50% in IBIT.

- Then 45% in T-bills and Notes

- Today, 1.7% money market fund, which act as collateral.

- Here, the options used are a combination of standardized exchange-traded options and FLEX options.

YBIT: top 10 holdings (Seeking Alpha)

It introduces them with the 3 mechanisms (“book of strategies” actively managed) operative introduced earlier: synthetic long, buys ATM calls (expiry 1 month – 1 year); covered call strategy sells OTM calls (strike 0-15% above the current price, expiry 1 month or less) and occasionally covered call spread strategy. Then the options are continuously “rolled” (rolling): when the contracts expire (naturally not expressed by the turnover which today is only 29%). Of these, the covered call strategy doesn’t seem to have a partial overlay today, which means there’s a fairly tight cap on the upside, which indicatively from my recalculations today stands at 35.37%, so very close.

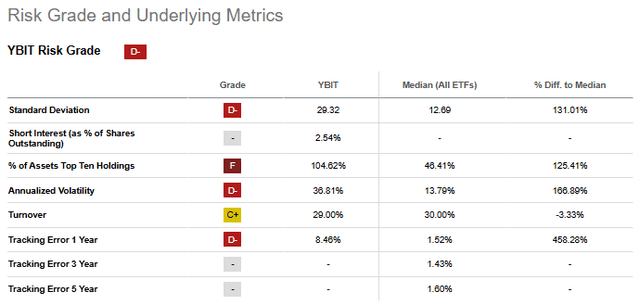

Risks

The risks one faces are multiple: the most relevant is the fact that there is an unbalanced risk-return trade off. In other words, the fund participates fully in declines, but has a close cap on rises. This makes the fund as volatile as the underlying, but in expansive contexts, not as profitable as the underlying.

YBIT: risk grade (Seeking Alpha)

Also called “call strategy risk” declared by the prospectus itself, with its numerical example (selling calls at 7% OTM every month, missing participation in the first 35% of cumulative rise over 5 months, with the possibility of losing money even against a cumulative rise of that magnitude) is the structural and official explanation of the phenomenon observed empirically

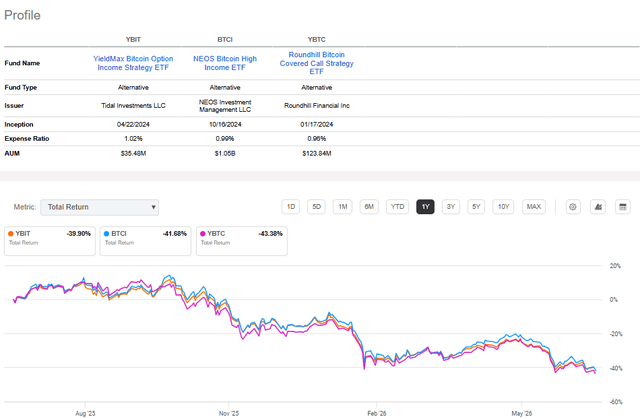

Peer Comparison

The main peers are identified as YBTC and the NEOS Bitcoin High Income ETF (BTCI); they are the two most used covered call solutions in the Bitcoin-underlying landscape.

YBIT: peer comparison (Seeking Alpha)

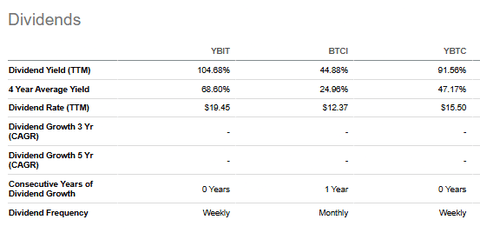

Although in total returns the 1-year difference is not so pronounced, when we move into the field of distributions we notice more marked differences. YBIT is the one among the two solutions with the (estimated) distribution rate, considering the latest distribution, higher than the other solutions, and probably for this reason also the one with the higher total expense ratio, although not so pronounced in comparison.

YBIT: dividends (Seeking Alpha)

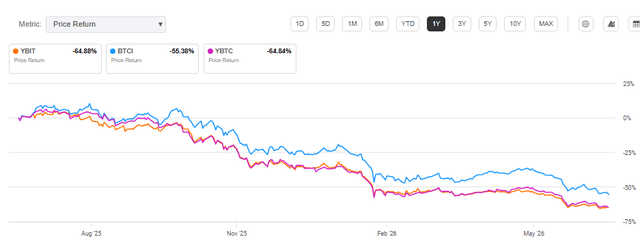

A more marked difference we see instead in price returns. And while here too between YBIT and the Roundhill Bitcoin Covered Call Strategy ETF (YBTC) there don’t seem to be particularly pronounced asymmetries in this phase of Bitcoin’s annual decline, on BTCI the matter changes, which seems to preserve capital better over 1Y. The reason lies in the cash flow objectives: BTCI has a declared target in the prospectus of 25-30% annually and implements it also through bear call spreads actively in declines, a flexibility declared and different from that of YBIT.

YBIT: price return (Seeking Alpha)

Pros and Cons

In light of this, there are some advantages worth mentioning when talking about YBIT:

- Generation of high income even in flat or bearish markets and clearly due to richer premiums in high volatility phases

- Declared flexibility of the strategy: the possibility of alternating between classic/deep ITM synthetic long, simple covered call/covered call spread, in theory allows the manager to better adapt to different market conditions.

But it would be impossible not to mention the negative sides as well; one in particular is identified:

- Like other covered call ETFs, it has a structural cap on the upside that generates a clear Path dependency that potentially separates its total return from that of the underlying (IBIT in this case).

This article answers three main questions about YBIT:

- What is YBIT’s objective and how is it constructed?

- What risks accompany holding YBIT?

- Which investors is YBIT most suitable for?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.